If you ever got a loan, you probably saw the words “Annual Percentage Rate (APR) on your paperwork. Did you ever try to figure it out or calculate it yourself, and was it still confusing?

If you need to understand it because now you’re making a home purchase learn what APR is, how to calculate it quickly, and why it is important.

What is The Definition of APR (Annual Percentage Rate)?

Quick “Cheat Method” to Calculate Your APR

APR is the True Cost of Your Loan

What Fees Are Included in an APR?

When Does it Make Sense to Pay Down For Points?

Why the APR Should Not Be Your End-All Tool in Decision Making

APR is the annual rate you are charged for borrowing a mortgage loan, expressed as a single percentage number that represents the actual yearly cost of borrowing over the term of your loan. APR includes the closing costs you are charged to attain your loan and the interest rate that you pay.

While the APR should not be the end-all tool for decision-making, it is a useful reference to gain a broad snapshot of the true cost of your loan. Fortunately, this is not too difficult to figure out.

Let me share a calculation method used to find an APR for a 15, 20, or 30-year fixed loan, without the use of the internet, armed only with a simple everyday calculator.

a) Lender origination fee b) Other closing costs |

$4,000 + $3,000 $7,000 |

|

30 years

x 12 months 360 months |

|

360 ÷ $7,000 =

19.44 |

|

19.44 ÷ 100 =

0.1944 |

|

4.00% |

|

4.0000%

+ 0.1944% 4.1944% |

|

4.1944% |

When getting a mortgage, you’ll be quoted an interest rate, which is the cost of borrowing the money. For example, a $300,000 loan multiplied by a 4% rate costs you $12,000 in interest per year.

But wait, there are additional fees you are charged to attain your loan. In the “Cheat Method” above, you’ll notice $4,000 in origination fees and $3,000 in closing costs.

When you combine these total closing costs with the interest rate charge, you come up with an APR, which is the true annual cost of your loan.

Note: the above cheat method only estimates your APR reliably for fixed loans between 15 and 30 years.

To accurately determine your APR, it actually requires some complicated math. Use this APR Calculator to easily determine what your APR is without having to rely on the lender to disclose it.

Tip: The federal Truth In Lending Act (TILA) requires that your lender disclose important terms of credit for the real estate mortgage you applied for, such as the APR. Additionally, TILA will include your finance charges to be paid, monthly payment, and whether or not you can repay your loan early without a penalty.

The fees that are included in an APR are:

Remember that your APR will be higher than your interest rate because it includes all those costs.

The word variable means that the rate can fluctuate at any given time to an index. In a market where interest rates go up and down, you end up paying more if rates are up, and if it goes down, you end up paying less.

When you get a variable APR, the lender will choose a specific benchmark to which to index the base interest rate.

Tip: Remember that the variable APR follows the U.S. Prime Rate, and it can change with the market.

One of the best ways to help you get a lower APR is by working on having a better credit score. Another way is by paying for discount points.

Remember that buying points are optional, and only do it if you have the money. With this option, you can also reduce your payment.

Typically a lender will allow you to buy a percentage from half of a point to 1% of the loan amount.

Tip: If you still need to decide about buying down points, make sure you ask your loan officer for help in giving different options you can compare.

Getting caught up in the Mortgage APR can be overwhelming. APR is a useful tool when shopping which lenders to use. However, remember that the fees lenders use to calculate your APR can vary. Therefore, the APR is an important number but should be one of many numbers you rely on.

Remember that your monthly mortgage payments are only based on the interest rate quoted and not the APR.

To get a complete picture, review your Loan Estimate, which will show you the interest rate and estimate all the closing costs required to close your loan.

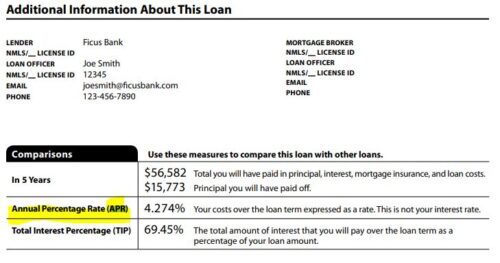

In your loan estimate, you will also see your APR, which we show you in the picture above.

In your loan estimate, you will also see your APR, which we show you in the picture above.

If you have any questions about your APR, please let us know. We are here to help your homeownership come to reality.