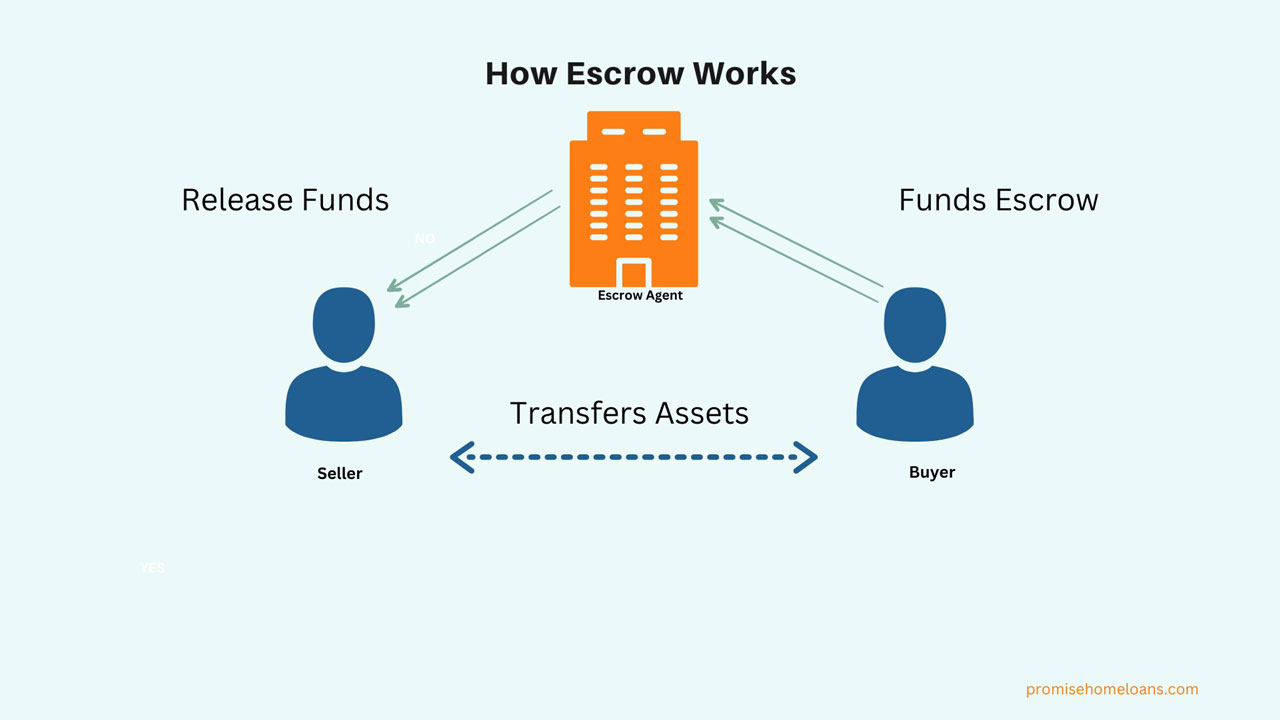

Escrow is a neutral third party that safeguards your real estate and mortgage transactions. They ensure all parties are in agreement before releasing money and closing.

Suppose you’re like the millions of people who buy and sell real estate, get a new mortgage, or refinance an existing mortgage each year. In that case, you will rely on an escrow company that protects and facilitates the exchange of monies and documents between all parties involved.

What is an Escrow Account for Your Mortgage?

Who manages Escrow in Mortgages?

What Are the Duties of Escrow?

How Can You Close Escrow On-Time?

Escrow provides what is known as a settlement service. Escrow companies are regulated neutral third parties who hold all monies involved in a transaction and release money only when conditions within the contracts are performed and met by two or more parties involved in the deal. Escrow ensures all this happens at the same time. Until that point, no party is fully committed.

Definition of Settlement Services as defined by law:

Settlement services include “any service provided in connection with a real estate settlement including, but not limited to, the following: title searches, title examinations, the provision of title certificates, title insurance, services rendered by an attorney, the preparation of documents, property surveys, the rendering of credit reports or appraisals, pest and fungus inspections, services rendered by a real estate agent or broker, the origination of a federally related mortgage loan (including, but not limited to, the taking of loan applications, loan processing, and the underwriting and funding of loans), and the handling of the processing, and closing of settlement.” 12 USCS § 2602

In other words, escrow ensures all parties agree before any deal closes.

When getting a mortgage, you will notice that many lenders require an escrow account to be set up to pay for property taxes and homeowners insurance.

Because your home is the bank’s collateral, the lender needs to protect your home from default due to missed property tax payments or catastrophic loss from lack of insurance coverage.

An escrow account holds your money and pays the tax collector and insurance company when payments are due. This is an easy way for homeowners to manage property taxes and insurance premiums for their homes.

TIP: Given a choice, many borrowers like using escrow as well! It helps spread tax bills and insurance premiums over monthly mortgage payments rather than having to pay for it as one large lump sum.

TIP: Paying your property taxes and insurance is your responsibility, even if you use an escrow account. Follow up and ensure that escrow funds are dispersed as agreed during the transaction.

If you open an escrow account after completing your mortgage transaction, the lender’s mortgage servicing company will manage the account. They will be responsible for paying your tax bills and insurance for you.

Depending On Your State, You Will Either Use an Escrow Company or a Settlement Company

Escrow companies and settlement companies function in the same way with the same duties.

Depending on your state, you may use a settlement company instead of an escrow company. Some states will even use attorneys or the Sheriff for certain settlement services. It can also vary from county to county within the same state.

In this post, we interchange the terms escrow company and settlement company.

The escrow is responsible for closing your loan after all conditions are met. This includes, but is not limited to, the following:

TIP: Escrow companies do not make lending decisions. They are responsible for following the rules agreed upon by all parties involved.

Escrow Is Responsible For One of the Most Important Documents: the HUD-1 Statement

The HUD-1, also known as a Settlement Statement, is a form the escrow agent uses that itemizes all charges you must pay for the mortgage transaction. The HUD-1 is prepared and finalized when loan documents are ready to sign to close your loan. The HUD-1 gives you a complete summary of all incoming and outgoing funds.

The HUD-1 includes the following items:

TIP: Be sure to review the HUD-1 or settlement statement carefully. It is the final statement of all the finances related to your transaction.

Other Important Documents Escrow is Responsible For

When signing loan documents on a new purchase or refinance, make sure you request the deed, note, and settlement statement to review in advance of signing. Pay close attention to these documents and make sure all the information is correct and exactly as agreed upon with your lender.

The cost of escrow varies depending on the type of transaction, the loan amount, and the number of parties involved. Typically, you can expect escrow to cost around 1%-2% of the purchase price in a real estate purchase or loan amount in a refinance.

Here is an example of the escrow cost:

If you buy a home with a sales price of $800,000, the escrow fee will be $8,000-$16,000.

In addition to the escrow fee, you may also incur incidentals such as:

Escrow is a detailed and well-defined process. There are natural timeframes escrow will follow, either due to law or custom. That being said, escrow can become delayed due to the action or inaction of multiple parties. Here is how you can help escrow close on time:

Follow All Instructions Quickly

Make sure to supply the required documents and signatures as quickly as possible and early in the day to your escrow company.

Monitor On-Site Inspections

Your transaction will likely require on-site inspections such as an appraisal or home inspection. Be sure you or your agents arrange these appointments quickly and with a company that can meet your deadline.

Communicate Regularly

It’s a mistake to sit back and wait. Communicate with all your mortgage professionals regularly and ask questions if you are unclear or anything doesn’t make common sense.

Review the escrow instructions

When the escrow company sends you the instructions, ensure your name and all other information are correct.

The buyer or the seller can pay the escrow fee, but this will depend on how you negotiate the costs. It’s typical for both parties to pay the escrow costs.

The moment a homebuyer makes an offer on a home and the seller accepts the offer is when the escrow period begins. The escrow period is typically 30-45 days, but it can be longer, depending on how long it takes to close the property.

Escrow Works for You!

Escrow companies are comprised of skilled and experienced people. Use your escrow professional to answer questions important to you about the closing process of your loan. If you’re not comfortable signing any documents until you have more information, that is your right.